Mantra & Co. - Advocate & Tax Consultant

Income Tax Compliance: From Return Filing to Notices and Appeals – A Practical Overview

Introduction

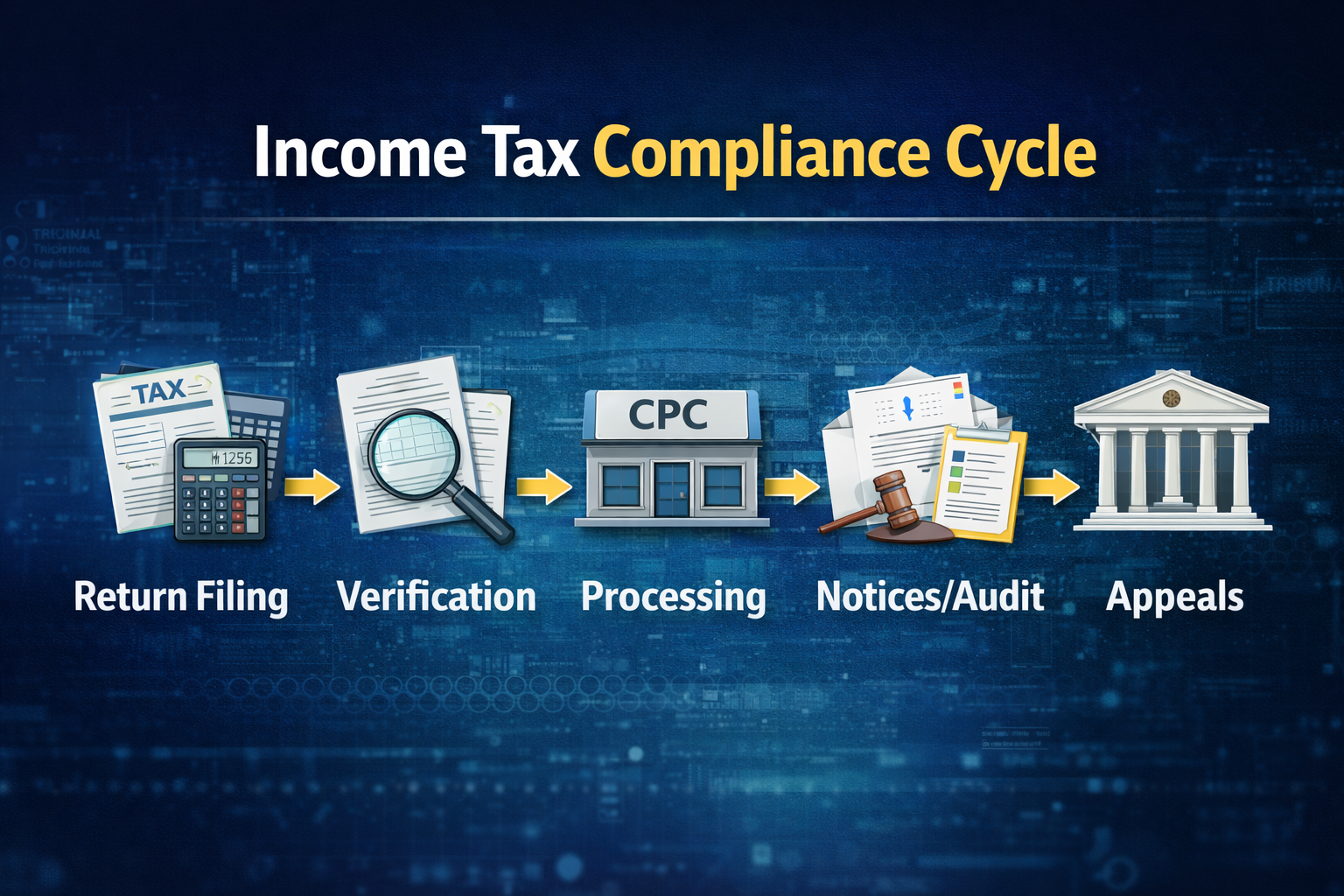

Income tax compliance in India is often misunderstood as a one-time activity limited to filing the income tax return. In reality, return filing is only the beginning of a broader compliance process that includes verification, communication with the tax department, and, where necessary, appellate remedies.

This article explains the income tax compliance framework in a simple and practical manner, covering return filing, notices, and appeals from an academic and informational perspective.

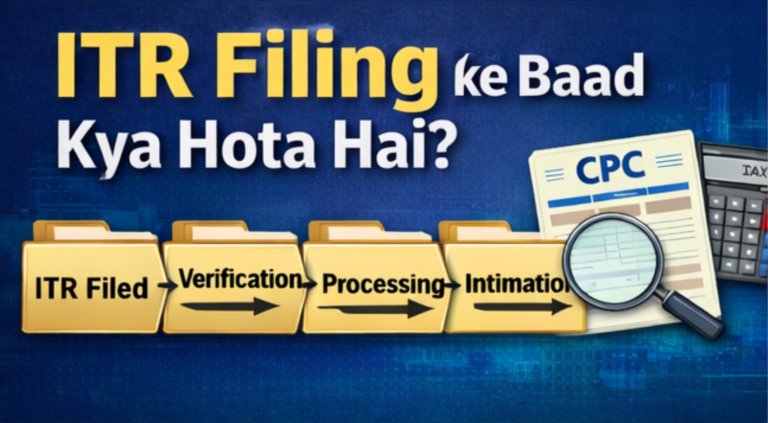

Watch the Complete Video Explanation on Income Tax Compliance

In this detailed video, we explain the complete Income Tax Compliance process — from Income Tax Return filing to scrutiny notices, reassessment proceedings, and appeal procedures in India. This practical overview will help you understand how the tax assessment system works after filing your ITR.

This video provides a structured understanding of the Income Tax compliance cycle, including return processing under section 143(1), scrutiny notices under section 143(2), reassessment proceedings, and the appeal framework available to taxpayers.

If you are a commerce student, tax professional, or business owner looking to understand the Income Tax assessment and notice handling process in India, this video offers practical clarity beyond theoretical concepts.

For a detailed written explanation, continue reading the full article below.

Return Filing: The First Step

Filing an income tax return is a statutory requirement through which a taxpayer discloses income details and calculates tax liability. Once the return is filed, it is processed by the Income Tax Department using automated and manual verification systems.

Return filing should therefore be viewed as the starting point of compliance, not its conclusion.

Post-Filing Verification and Processing

After submission, the return is verified using available data such as tax deducted at source (TDS), advance tax payments, and other financial information reported to the department. Any mismatch between the filed return and available data may lead to adjustments or requests for clarification.

Such verification is a routine part of the compliance process and does not automatically indicate any default by the taxpayer.

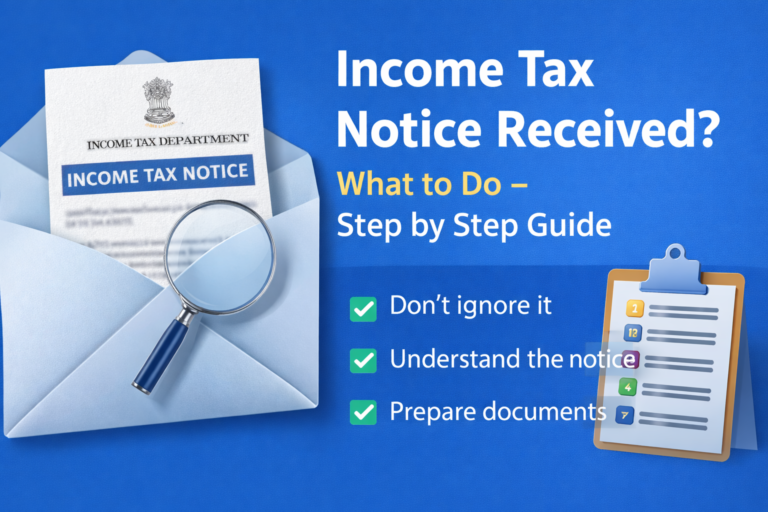

Income Tax Notices: Practical Understanding

An income tax notice is a formal communication issued to seek clarification, additional information, or compliance with statutory provisions. Notices are generally time-bound and require an appropriate response supported by facts and documentation.

It is important to understand that the issuance of a notice does not necessarily result in penalties or adverse consequences. Each notice is examined based on the facts of the case and applicable legal provisions.

Appeals: A Legal Remedy

If a taxpayer disagrees with an assessment or decision of the tax authorities, the Income Tax Act provides a structured appeal mechanism. Appeals must be filed within prescribed timelines and are decided based on facts, evidence, and applicable law.

The outcome of an appeal is case-specific and depends on proper presentation of facts and legal grounds.

Conclusion

Income tax compliance is a continuous and structured process that extends beyond return filing. Understanding the stages of verification, notice handling, and appeals helps taxpayers and students approach compliance with clarity and confidence.

Disclaimer: This article is for informational purposes only and does not constitute legal or tax advice. The views expressed are based on the current understanding of law and portal functionality as on the date of publication. Readers are advised to seek professional advice before taking any action.

If you have any general query or wish to understand the subject better, you may share your question in the comments below.