Mantra & Co. - Advocate & Tax Consultant

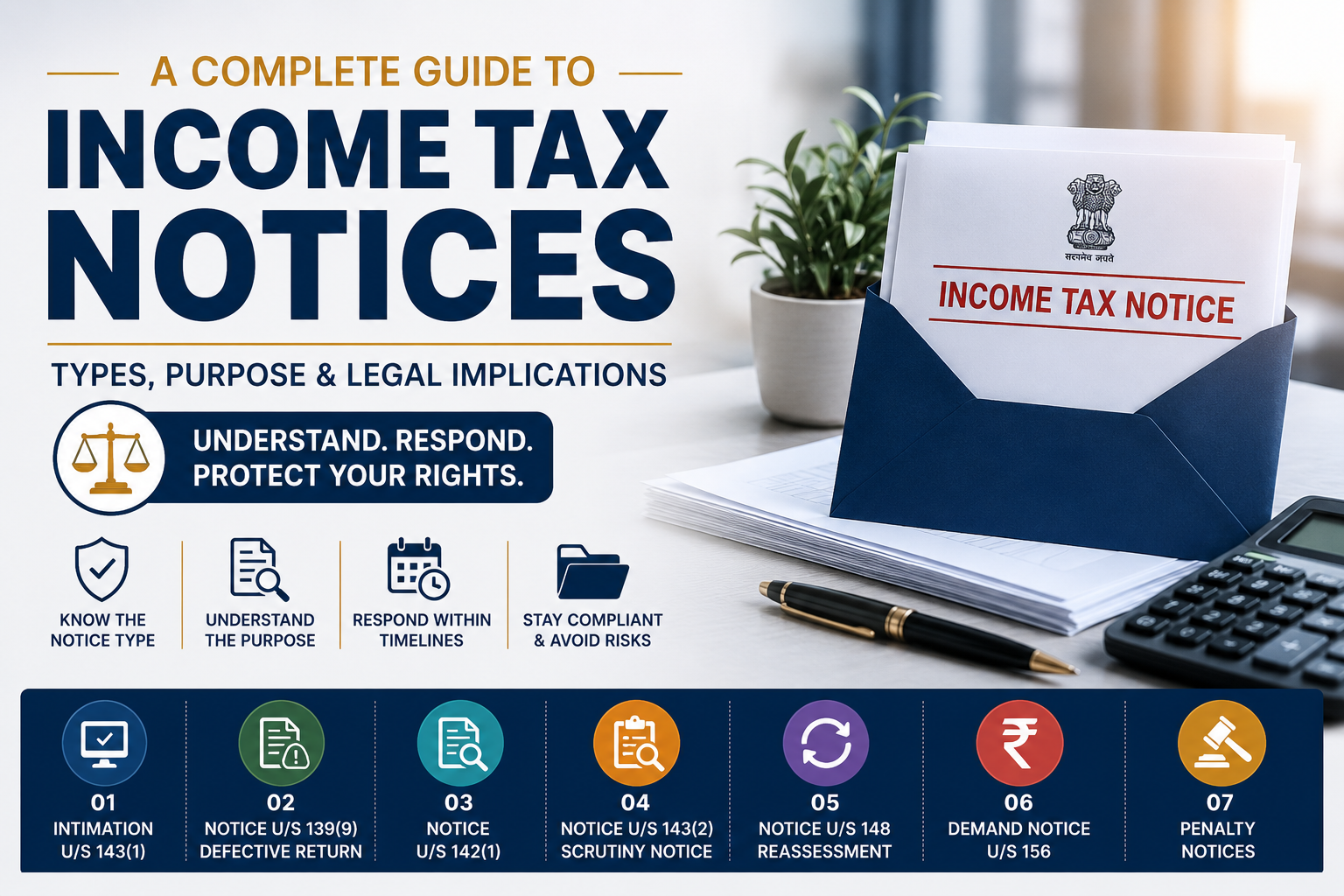

Classification of Income Tax Notices: Understanding the Types and Their Legal Implications

Introduction

Receiving an Income Tax notice often creates unnecessary anxiety among taxpayers. However, not every notice indicates wrongdoing or serious legal exposure.

In many cases, notices are automated communications triggered by data validation systems, routine scrutiny, or compliance checks. Understanding the type of notice received is the first step toward responding appropriately and strategically.

This article provides a structured overview of the major types of Income Tax notices issued under the Income Tax Act and explains their purpose, scope, and implications.

Watch the Complete Video Explanation

This topic has also been explained in detail in the video below. Watch for practical clarity and structured understanding

Is video, we explain the entire process that takes place after filing an Income Tax Return in a simple, practical, and fear-free manner.

Why Income Tax Notices Are Issued

Income Tax notices may be issued for various reasons, including:

- Data mismatch with AIS or Form 26AS

- Verification of deductions or exemptions

- Defective return filing

- Reassessment of escaped income

- Routine scrutiny selection

- Non-filing of return

Notices are part of the compliance framework and are legally recognized communication tools of the department.

Major Types of Income Tax Notices

1. Intimation under Section 143(1)

| Nature | System-generated communication issued after return processing. |

| Common Reasons | • Arithmetic corrections • Incorrect claim adjustments • Deduction mismatch corrections • Tax demand or refund determination |

| Scrutiny Assessment? | No. This is a processing intimation and not a scrutiny notice. |

| Action Required | Review the computation carefully and file a rectification request if any discrepancy is identified. |

Receiving an Intimation under Section 143(1) does not automatically indicate tax non-compliance or scrutiny. It is a routine communication issued after return processing. Taxpayers should carefully verify any adjustments, tax demand, or refund details and take corrective action where necessary.

2. Notice under Section 139(9) – Defective Return

| Nature | Issued when the Income Tax Return (ITR) filed by the taxpayer is considered defective or incomplete under the provisions of the Income Tax Act. |

| Common Reasons | • Incorrect ITR form selection • Missing schedules or mandatory disclosures • Incomplete financial information • Non-reporting of mandatory disclosures • Mismatch between reported income and supporting details |

| Scrutiny Assessment? | No, This is a procedural notice issued to enable correction of defects identified in the return and does not initiate scrutiny assessment proceedings. |

| Action Required | The identified defects must be rectified and the corrected return submitted within the prescribed time limit. Failure to comply may result in the return being treated as invalid. |

A notice under Section 139(9) is primarily a compliance-related communication intended to correct deficiencies in the return filed. Prompt rectification helps maintain the validity of the return and prevents avoidable compliance issues or delays in processing.

3. Notice under Section 142(1)

| Nature | Issued by the Income Tax Department to obtain additional information, documents, or explanations from the taxpayer for the purpose of assessment or verification. |

| Common Reasons | • Clarification of specific entries reported in the Income Tax Return (ITR) • Submission of books of accounts and supporting records • Explanation of high-value or unusual transactions • Verification of income, deductions, exemptions, or financial disclosures |

| Scrutiny Assessment? | Not necessarily. However, this notice may be issued before or during assessment proceedings and can form part of the verification process undertaken by the department. |

| Action Required | Carefully review the information requested and submit accurate documents, records, and explanations within the prescribed timeline. Non-compliance may result in further proceedings or adverse assessment consequences. |

A notice under Section 142(1) is a verification-oriented communication issued by the Income Tax Department to gather additional information from the taxpayer. Timely and accurate submission of the requested documents helps facilitate smooth assessment proceedings and reduces the risk of unnecessary disputes or compliance issues.

4. Notice under Section 143(2) – Scrutiny Notice

| Nature | Issued when the Income Tax Return (ITR) filed by the taxpayer is selected for detailed examination by the Income Tax Department to verify the accuracy and completeness of the information reported. |

| Common Reasons | • Verification of income declared in the return • Examination of deductions, exemptions, and tax benefits claimed • Review of capital gains and investment transactions • Validation of business transactions, expenses, and supporting records • Assessment of overall tax compliance |

| Scrutiny Assessment? | Yes. This notice signifies the commencement of scrutiny assessment proceedings and indicates that the return is being subjected to detailed verification by the department. |

| Action Required | A comprehensive and well-documented response should be prepared along with all relevant supporting documents, books of accounts, financial records, and explanations. Timely compliance is essential to avoid adverse assessment outcomes. |

A notice under Section 143(2) is one of the most significant Income Tax notices as it initiates scrutiny assessment proceedings. While it does not automatically imply wrongdoing, taxpayers should respond carefully with complete documentation and factual explanations to substantiate the income, deductions, and transactions reported in the return.

5. Notice under Section 148 – Reassessment

| Nature | Issued when the Income Tax Department has reason to believe that certain income chargeable to tax has escaped assessment and requires reassessment under the provisions of the Income Tax Act |

| Typical Triggers | • Undisclosed or unreported income • Significant mismatch in information reported in AIS, Form 26AS, or other records • High-value financial transactions not disclosed in the Income Tax Return (ITR) • Information received from regulatory authorities, investigation agencies, or other external sources • New evidence indicating potential underreporting of income |

| Scrutiny Assessment? | No. This is a reassessment notice and not a regular scrutiny notice. However, it initiates reassessment proceedings that may result in the reopening of previously completed assessments. |

| Action Required | Carefully examine the reasons provided for reopening the assessment and prepare a detailed response supported by relevant documents, records, and explanations. Professional guidance may be advisable in complex reassessment matters. |

A notice under Section 148 is issued when the Income Tax Department believes that income may have escaped assessment. Since reassessment proceedings can reopen earlier completed assessments and have significant tax implications, taxpayers should review the notice carefully and respond with proper documentation and factual justification.

6. Demand Notice under Section 156

| Nature | Issued by the Income Tax Department when any tax, interest, fee, or penalty becomes payable by the taxpayer pursuant to an assessment, reassessment, rectification, or other proceedings under the Income Tax Act. |

| Common Reasons | • Communication of outstanding tax liability • Recovery of unpaid tax, interest, fee, or penalty • Formal demand for payment of dues determined by the department • Intimation of the amount payable and the prescribed payment timeline |

| Scrutiny Assessment? | No. A notice under Section 156 is not a scrutiny assessment notice. It is a demand notice issued after the determination of a tax liability or other amount payable under the Income Tax Act. |

| Action Required | Verify the demand raised by the department and review the underlying assessment order or computation. If the demand is correct, payment should be made within the prescribed period. If there is a disagreement, appropriate legal remedies such as rectification, appeal, or other available proceedings may be considered. |

A notice under Section 156 is a formal demand issued by the Income Tax Department for payment of tax, interest, fee, or penalty. Ignoring the notice may result in recovery proceedings, additional interest liabilities, or enforcement actions. Taxpayers should promptly verify the demand and take appropriate action within the prescribed timeline.

7. Penalty Notices

| Nature | Issued by the Income Tax Department to initiate penalty proceedings where a taxpayer is alleged to have failed to comply with specific provisions of the Income Tax Act or related compliance requirements. |

| Common Reasons | • Underreporting of income • Misreporting or concealment of income • Failure to comply with Income Tax notices or departmental directions • Non-maintenance or improper maintenance of prescribed books of accounts and records • Other specified defaults under the Income Tax Act |

Penalty notices can have significant financial implications, including monetary penalties for non-compliance with the Income Tax Act. However, the issuance of a penalty notice does not automatically result in a penalty. A timely and well-supported response can help explain the circumstances, establish compliance, and protect the taxpayer’s legal rights.

Strategic Approach to Handling Notices

Upon receiving any notice:

- Identify the section under which it is issued

- Understand whether it is processing, verification, or assessment related

- Check response timelines

- Review underlying facts and documentation

- Prepare a structured reply

Professional representation may be appropriate in scrutiny, reassessment, or penalty Structured cases.

Common Mistake to Avoid

Ignoring a notice is the most serious compliance error.

Non-response may lead to:

- Ex-parte orders

- Additional tax demands

- Penalty imposition

- Recovery proceedings

Timely response preserves legal rights and procedural safeguards.

Conclusion

Income Tax notices are structured legal communications, not automatic evidence of default. Proper classification and understanding of the notice type determine the response strategy.

Clarity, documentation, and procedural discipline are the keys to effective notice management.