Mantra & Co. - Advocate & Tax Consultant

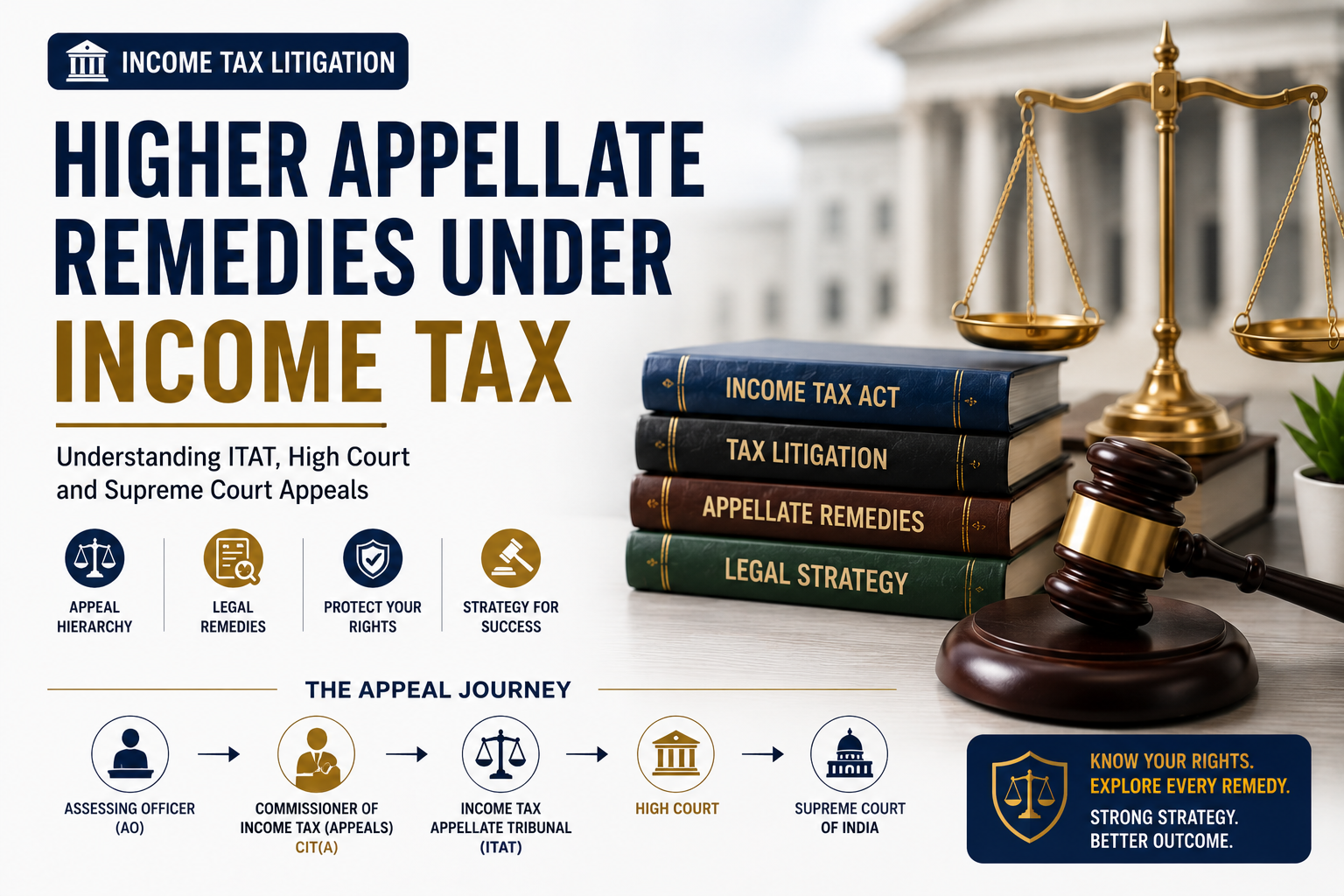

Higher Appellate Remedies Under Income Tax: Understanding ITAT, High Court and Supreme Court Appeals

Introduction

Many taxpayers believe that once an order is passed by the Commissioner of Income Tax (Appeals), the litigation process comes to an end. However, that is not always the case.

Under the Income Tax Act, there are multiple Higher Appellate Remedies under Income Tax available if either the taxpayer or the department is not satisfied with the appellate decision.

Tax litigation follows a structured hierarchy. Understanding this hierarchy is important because every appellate level has a different purpose, scope, and procedural requirement.

For business owners, taxpayers, students, and tax professionals, knowing what happens after CIT(A) can help in making better legal and compliance decisions.

Watch the Complete Video Explanation

For a better understanding of this topic, you can also refer to the detailed video explanation where the concepts are discussed step-by-step with practical insights and real-world context.

Understanding the Income Tax Litigation Hierarchy

Income tax disputes generally follow a structured litigation flow:

Assessing Officer (AO) → CIT(A) → ITAT → High Court → Supreme Court

This hierarchy ensures that tax disputes are reviewed at multiple levels where necessary.

It is important to understand one practical point:

Not every case reaches the Supreme Court.

Each appellate forum has its own jurisdiction, and only certain issues qualify for higher remedies.

This makes procedural understanding very important.

Income Tax Appellate Tribunal (ITAT): The Second Appeal

After an order of the Commissioner of Income Tax (Appeals), the next appellate remedy is generally before the Income Tax Appellate Tribunal.

The ITAT is an independent appellate authority where both:

- Taxpayer

- Income Tax Department

can file appeals.

Why is ITAT important?

The ITAT examines:

- Facts of the case

- Supporting evidence

- Legal provisions

- Interpretation of law

In many tax disputes, the ITAT’s order becomes the final finding on facts.

Example:

Suppose the Assessing Officer makes an addition for unexplained expenditure. The CIT(A) confirms that addition. If the taxpayer believes that important evidence was not properly considered, the matter can be challenged before ITAT.

Insight:

- Grounds of appeal should be drafted clearly

- Documents should be complete

- Evidence should be properly organized

Weak factual presentation can weaken the appeal.

High Court Appeal: Substantial Question of Law

After the ITAT stage, the next remedy may lie before the High Courts of India.

However, this stage is different.

Not every ITAT order can be challenged before the High Court.

The High Court generally entertains matters involving a Substantial Question of Law.

What does this mean?

It usually refers to:

- Important legal interpretation

- Conflict between judicial decisions

- Significant application of law

Simple factual disagreement is usually not enough.

Example:

If there is a dispute regarding interpretation of a deduction provision under the Income Tax Act and courts have differing views, the issue may qualify for High Court review.

Important Rule:

- Clearly identify the legal issue

- Frame the question of law properly

- Separate factual disputes from legal disputes

This stage requires careful legal structuring.

Supreme Court: Final Judicial Authority in Tax Matters

The Supreme Court of India is the highest judicial authority in the country.

It acts as the final appellate forum in significant tax disputes.

However, an important practical point is:

Every High Court matter does not automatically go to the Supreme Court.

Specific legal procedures and grounds must exist.

The Supreme Court usually deals with:

- Major legal controversies

- Constitutional questions

- National-level tax interpretation issues

- Important legal precedents

The judgments of the Supreme Court often guide tax administration across India.Practical Example:

If there is a nationwide issue regarding interpretation of a major tax provision affecting multiple taxpayers, the matter may reach the Supreme Court.

Can the Income Tax Department Also File an Appeal?

Yes.

A common misconception is that only taxpayers file appeals.

In reality, the Income Tax Department can also challenge appellate orders if it believes the decision is legally incorrect.

This means:

Appeal = Taxpayer OR Department

For example:

- Department may challenge relief granted by CIT(A)

- Department may challenge ITAT findings before High Court (if legal issues arise)

This makes the appellate system a two-way mechanism.

Why Strategy Matters in Higher Appellate Remedies

In higher appellate forums, simply having a grievance is not enough.

A strong appeal generally requires:

Facts + Law + Presentation = Strong Appeal

This means:

- Clear factual background

- Proper documentary evidence

- Correct legal interpretation

- Well-drafted grounds of appeal

- Clearly stated relief

In practice, many cases become weak not because of poor merits, but because of poor presentation.

Proper litigation strategy plays an important role.

Common Mistakes in Higher Tax Appeals

Many tax appeals face difficulty because of procedural and drafting mistakes.

| Mistake | What It Means | Possible Impact |

| Ignoring Limitation Period | Missing appeal deadlines | Appeal may become delayed or dismissed |

| Vague Grounds of Appeal | General or unclear legal objections | Weakens the legal challenge |

| Failure to Identify Legal Issues | Not distinguishing factual and legal matters | Higher forums may not admit the case |

| Incomplete Documentation | Missing supporting evidence or records | Reduces factual credibility |

| Emotional Drafting | Using unnecessary emotional or aggressive language | Weakens professionalism and legal clarity |

| Wrong Appellate Forum | Filing appeal without understanding hierarchy | Procedural complications and delays |

Insight:

In many tax disputes, procedural mistakes can damage a strong case.

Conclusion

The Higher Appellate Remedies under Income Tax provide taxpayers and the department with a structured mechanism for judicial review and fair hearing.

The appellate hierarchy—from ITAT to High Court and Supreme Court—ensures that both factual and legal disputes can be reviewed at appropriate levels.

However, understanding the correct forum, limitation periods, legal issues, and documentation requirements is essential. In tax litigation, strategy and compliance are often as important as the merits of the case itself.

Tax disputes are not only about liability—they are also about understanding the legal process properly.

Disclaimer

This article is for educational purposes only and should not be considered legal or tax advice.