Mantra & Co. - Advocate & Tax Consultant

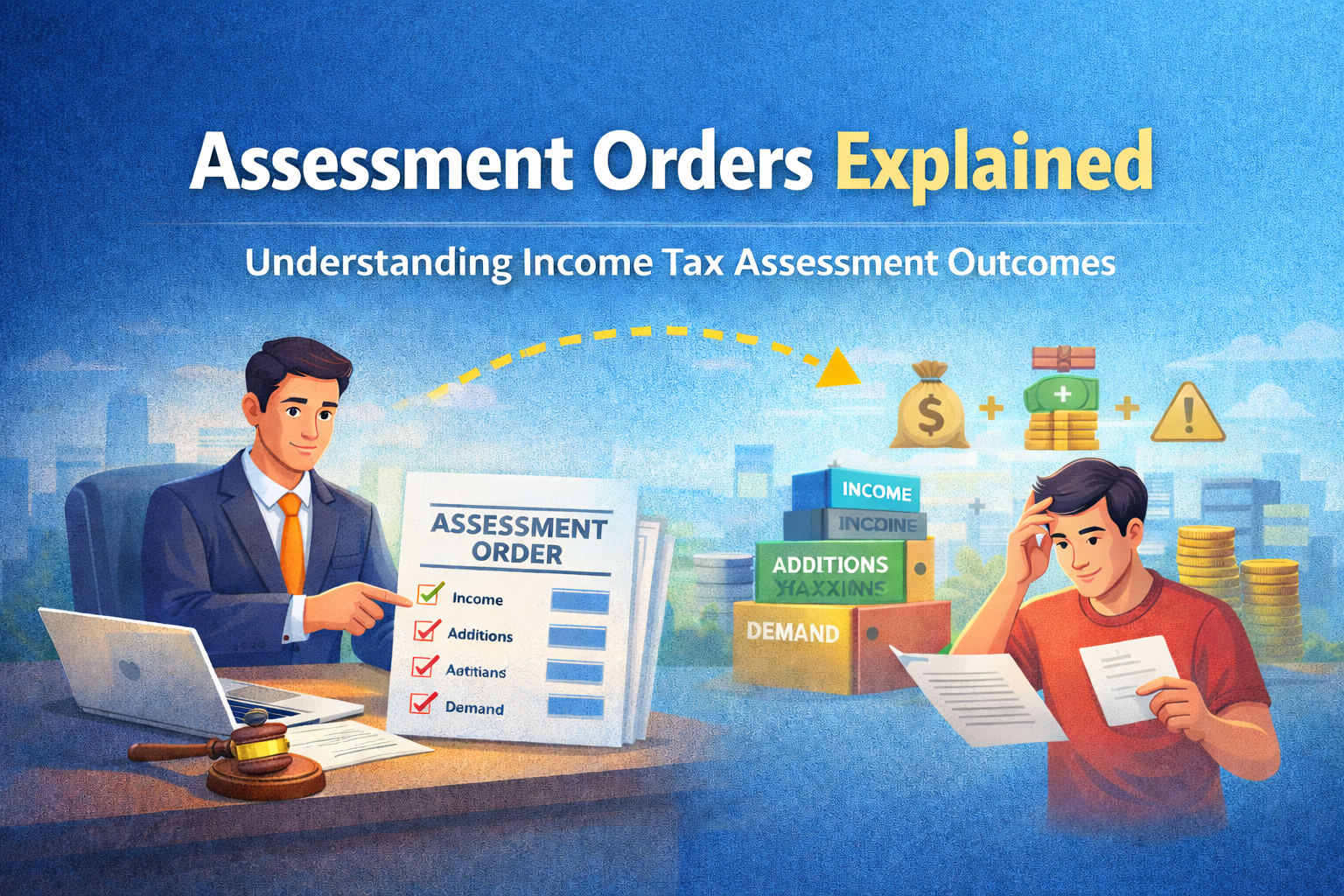

Assessment Orders Explained – Understanding Income Tax Assessment Outcomes

Introduction

Filing an Income Tax Return is only the beginning of the compliance process. After the return is processed and verified through the department’s automated systems and risk parameters, the Income Tax Department may initiate an assessment proceeding to examine the correctness of the return filed.

The outcome of such proceedings is communicated through an assessment order, which determines the final tax liability of the taxpayer for that assessment year.

Understanding assessment orders is essential for taxpayers, professionals, and students of taxation because it clarifies how the department evaluates income declarations and how disputes may arise.

This article explains the concept of assessment orders, their types, practical implications, and the taxpayer’s options after receiving such an order.

Watch the Complete Video Explanation

This topic has also been explained in detail in the video below. Watch for practical clarity and structured understanding

What is an Assessment Order?

An assessment order is a formal decision issued by the Assessing Officer (AO) after examining the taxpayer’s return, documents, and explanations during assessment proceedings.

The order determines:

• Total taxable income

• Tax liability

• Additions or disallowances made by the department

• Interest, penalties, or refunds, if applicable

In simple terms, the assessment order represents the final conclusion of the tax department regarding a taxpayer’s income for that year.

Types of Assessment Under the Income Tax Act

Assessment orders may arise under different types of assessment proceedings.

1. Summary Assessment (Section 143(1))

This is the automated processing of the return conducted by the Central Processing Centre (CPC).

The system verifies:

• Mathematical accuracy

• TDS credits

• AIS information

• Claim mismatches

The result is communicated through an Intimation under Section 143(1).

Possible outcomes:

• Refund issued

• No demand / no refund

• Tax demand raised due to adjustment

2. Scrutiny Assessment (Section 143(3))

In certain cases, the department selects returns for detailed examination.

During scrutiny assessment:

• Notices are issued to the taxpayer

• Supporting documents are requested

• Explanations for transactions are sought

After reviewing all submissions, the Assessing Officer issues an assessment order under Section 143(3).

The officer may:

• Accept the return

• Make additions to income

• Disallow certain deductions or expenses

3. Best Judgment Assessment (Section 144)

If the taxpayer fails to comply with notices or does not provide the required information, the Assessing Officer may complete the assessment based on available information.

This is known as Best Judgment Assessment.

In such cases:

• The officer estimates income

• Additions may be higher

• Demand may arise

This situation often occurs due to non-compliance with notices.

Common Outcomes of an Assessment Order

After completing the assessment, the officer may reach different conclusions.

1. Return Accepted

The department agrees with the taxpayer’s return and no changes are made.

2. Additions to Income

The officer may increase the taxable income due to:

• unexplained credits

• disallowed expenses

• mismatch in AIS/TDS data

3. Tax Demand

If additional tax liability arises after assessment, a demand notice is issued.

4. Refund

In some cases, excess tax paid may result in a refund.

Why Do Assessment Orders Become a Dispute?

Assessment orders may lead to disputes due to:

• Different interpretation of tax laws

• Lack of documentation

• Incorrect classification of income

• Additions made by the department

When taxpayers disagree with an assessment order, they may challenge it through the appeal process.

What Should a Taxpayer Do After Receiving an Assessment Order?

Once an assessment order is received, the taxpayer should carefully review the following:

• Reasons for additions or disallowances

• Supporting evidence relied upon by the department

• Tax demand raised

Based on the analysis, the taxpayer may choose to:

• accept the order and pay demand

• file a rectification application

• file an appeal before the Commissioner of Income Tax (Appeals)

Proper professional advice is often required at this stage to evaluate the best course of action.

Conclusion

Assessment orders play a crucial role in the tax administration system as they represent the final determination of a taxpayer’s income after examination by the tax authorities.

Understanding how assessment proceedings work and how assessment orders are passed helps taxpayers and professionals handle tax disputes more effectively.

Awareness of the process also enables taxpayers to respond appropriately and protect their legal rights when disagreements arise.

Tax ko samajhna mushkil nahi hai,

system ko samajhna zaroori hai.

Disclaimer: This article is for informational purposes only and does not constitute legal or tax advice. The views expressed are based on the current understanding of law and portal functionality as on the date of publication. Readers are advised to seek professional advice before taking any action.

If you have any general query or wish to understand the subject better, you may share your question in the comments below.