Mantra & Co. - Advocate & Tax Consultant

Right to Appeal Under Income Tax: Understanding Demand Notice and Appeal Process in India

Introduction

In the Indian tax system, receiving an assessment order or a demand notice from the Income Tax Department can create confusion and concern for many taxpayers. However, it is important to understand that the law does not leave taxpayers without remedies.

One of the most important safeguards available under the Income Tax Act is the Right to Appeal under Income Tax. If a taxpayer believes that an assessment order is incorrect, excessive, or based on an improper interpretation of law, they have the legal right to challenge it before a higher authority.

Understanding how the appeal process works can help taxpayers, business owners, and students navigate tax disputes more confidently and avoid unnecessary complications.

Watch the Complete Video Explanation

For a better understanding of this topic, you can also refer to the detailed video explanation where the concepts are discussed step-by-step with practical insights and real-world context.

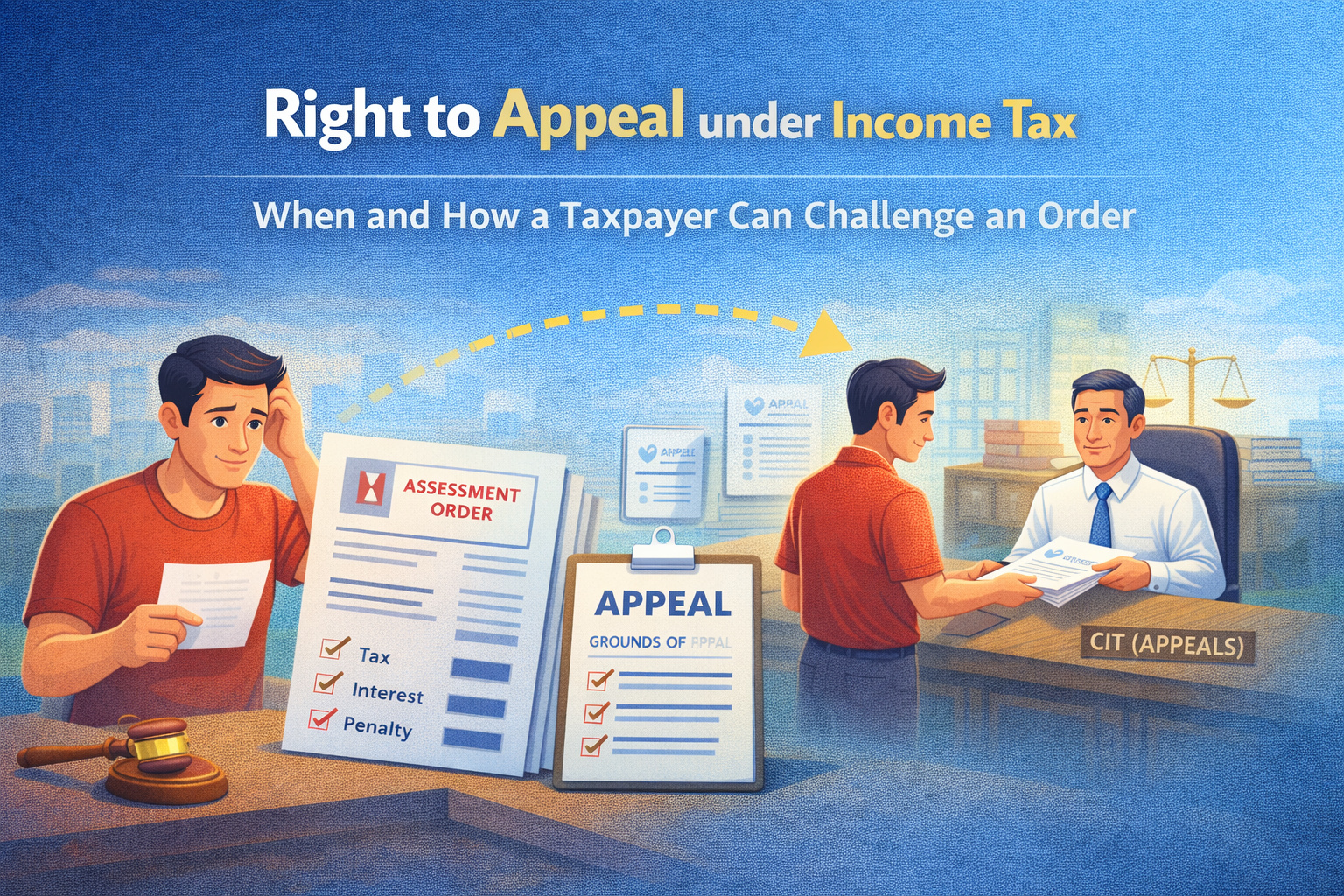

What is the Right to Appeal Under Income Tax?

The Right to Appeal under Income Tax allows a taxpayer to seek a review of an order passed by the Income Tax Department when they disagree with it.

The process generally works like this:

Assessment Order → Disagreement → Appeal

In simple words, if a taxpayer feels that the tax officer has made an incorrect addition, denied a valid deduction, or misinterpreted the law, they can approach the appellate authority for review.

This mechanism helps maintain fairness, transparency, and accountability within the tax system.

Purpose of Filing an Income Tax Appeal

The appeal mechanism exists to provide taxpayers with an opportunity to present their side.

Why is it important?

- It ensures fair treatment under tax law.

- It allows correction of errors in assessment orders.

- It provides a structured legal remedy.

- It prevents arbitrary tax demands.

For example, if a taxpayer’s legitimate business expense is disallowed during assessment, the appeal process can help get that issue reviewed.

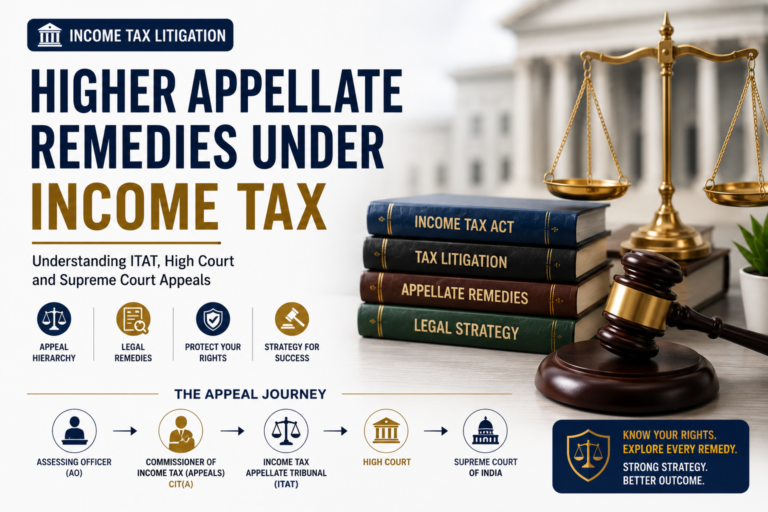

First Level of Appeal: Commissioner of Income Tax (Appeals) – CIT(A)

The first appellate authority in most income tax matters is the Commissioner of Income Tax (Appeals).

When a taxpayer disagrees with an assessment order, the appeal is usually filed before CIT(A).

The Commissioner reviews:

- The assessment order

- The taxpayer’s written submissions

- Supporting documents

- Relevant provisions of law

- Judicial interpretations, where applicable

This review is an important step in resolving disputes without moving directly into higher litigation.

What Happens During the Appeal Process?

Once an appeal is filed, the appellate authority examines the matter in detail.

The CIT(A) may:

1. Confirm the Order

If the authority finds the assessment correct.

2. Modify the Order

If certain additions or disallowances need correction.

3. Cancel the Order

If the order is found legally or factually incorrect.

This means the original tax demand may remain, reduce, or even be cancelled depending on the facts of the case.

Understanding Demand Notice Under Section 156

A Demand Notice is issued under Section 156 of the Income Tax Act when additional tax becomes payable after assessment.

This notice informs the taxpayer about the amount payable.

Usually, the taxpayer gets 30 days to make the payment.

However, ignoring a demand notice can lead to recovery proceedings.

Possible recovery actions may include:

- Bank account attachment

- Property attachment

- Adjustment of tax refunds

- Recovery through legal proceedings

This makes it essential to understand whether the demand is correct and act within time.

Time Limit for Filing Appeal Against Assessment Order

One of the most important compliance points in the appeal process is the time limit.

Generally, a taxpayer has 30 days from the date of receiving the order to file an appeal.

Timeline:

Order Received → 30 Days → Appeal Filing

If the appeal is filed after the prescribed period, a condonation of delay request may be required, along with valid reasons for the delay.

Delays without proper explanation may affect the appeal process.

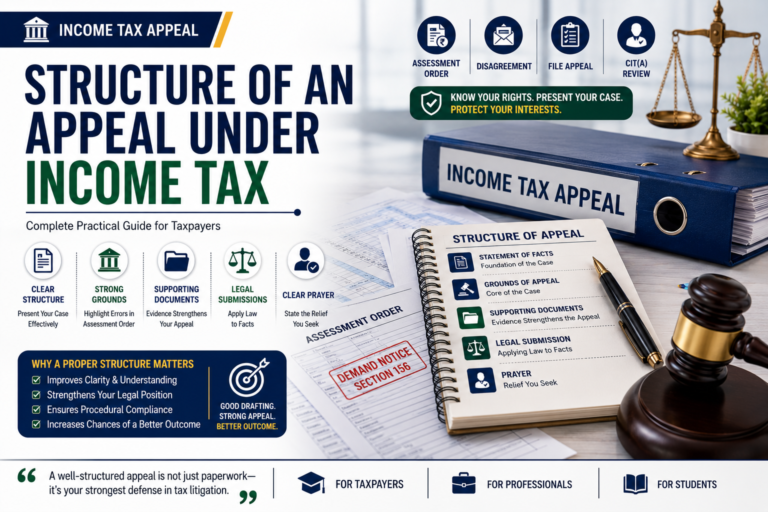

Grounds of Appeal: Why They Matter

A strong appeal begins with properly drafted Grounds of Appeal.

These are the specific reasons explaining why the taxpayer believes the order is incorrect.

Common grounds may include:

- Wrong addition to taxable income

- Incorrect rejection of deductions

- Disallowance of business expenses

- Wrong interpretation of tax provisions

- Incorrect tax calculation

Example:

Suppose a taxpayer claims depreciation on machinery, but the assessing officer disallows it despite valid records. This could become a ground of appeal.

Clear and precise grounds improve the clarity of the case.

Common Mistakes Taxpayers Make During Appeal Filing

Many taxpayers weaken their case because of avoidable errors.

Common mistakes include:

- Missing the appeal deadline

- Filing incomplete documents

- Drafting vague grounds of appeal

- Ignoring demand notices

- Not maintaining supporting evidence

- Misunderstanding legal provisions

Therefore, timely action and proper understanding are important.

Importance of Proper Representation in Tax Litigation

Tax litigation often involves both factual and legal interpretation.

Professional representation can help in:

- Preparing proper grounds of appeal

- Structuring facts clearly

- Presenting documentary evidence

- Explaining applicable legal provisions

A properly presented case can improve clarity and procedural compliance.

Conclusion

The Right to Appeal under Income Tax is an important legal safeguard that ensures taxpayers have an opportunity to challenge incorrect assessments and demand notices. Understanding the appeal process, timelines, required documents, and grounds of appeal can make a significant difference in handling tax disputes effectively.

Whether it is a demand notice under Section 156 or an assessment order involving disputed additions, timely action is essential. Tax compliance is not only about paying taxes—it is also about understanding your legal rights within the system.

Disclaimer

This article is for educational purposes only and should not be considered legal or tax advice.