Mantra & Co. - Advocate & Tax Consultant

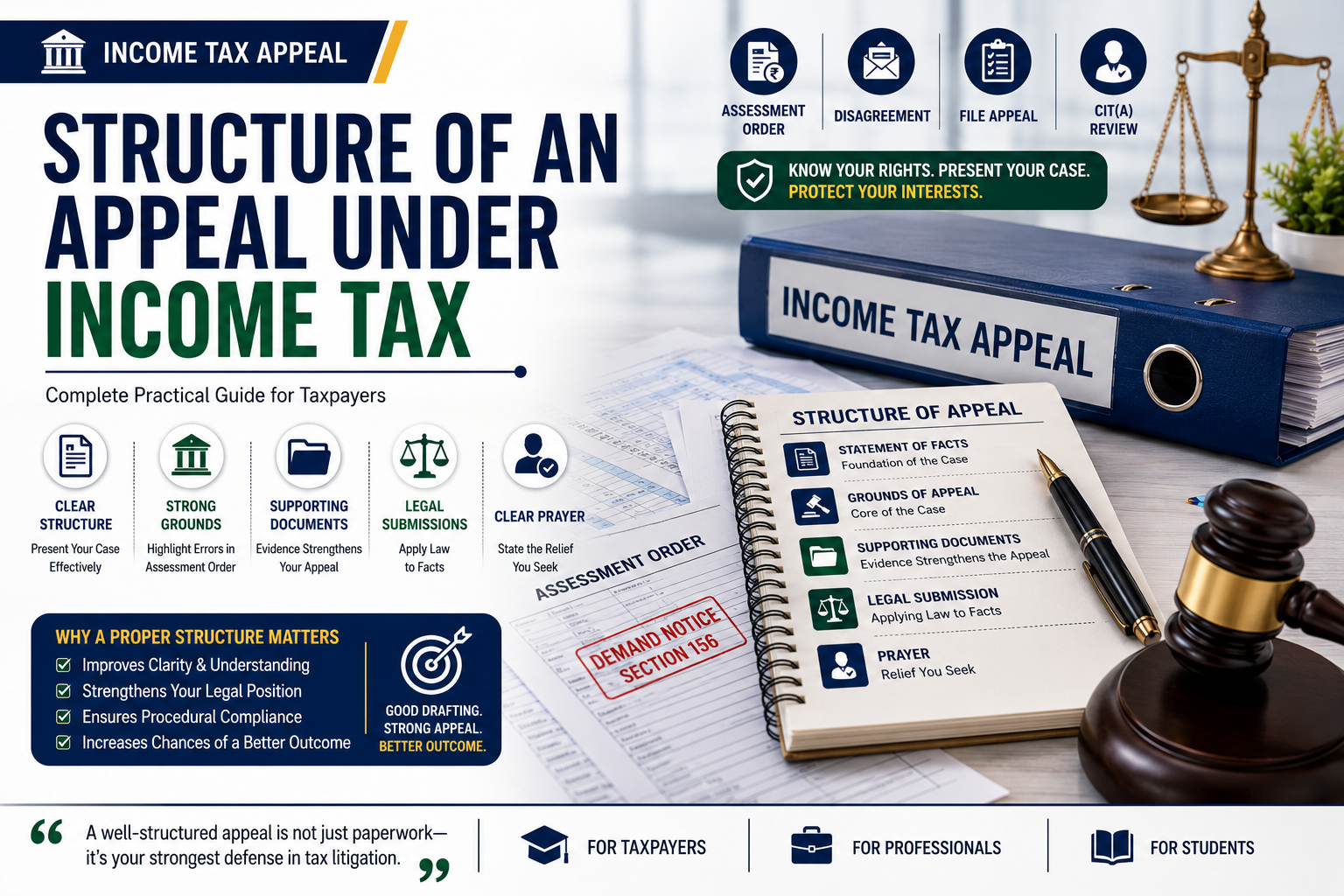

Structure of an Appeal Under Income Tax: Complete Practical Guide for Taxpayers

Introduction

Filing an appeal under the Income Tax Act is not just a procedural formality. It is a structured legal process where the taxpayer presents their case before the appellate authority in a clear, organized, and evidence-backed manner.

Many taxpayers believe that filing an appeal simply means submitting a form. However, in practice, the Structure of an Appeal under Income Tax plays a critical role in how effectively a case is presented.

If the appeal is poorly drafted, lacks proper documentation, or contains vague grounds, it can weaken the case significantly. Therefore, understanding the practical framework of appeal drafting is essential for taxpayers, business owners, students, and tax professionals.

Watch the Complete Video Explanation

This topic has also been explained in detail through our video session. Watch the complete explanation to understand how internships and professional courses work together to build practical expertise in accounting and taxation

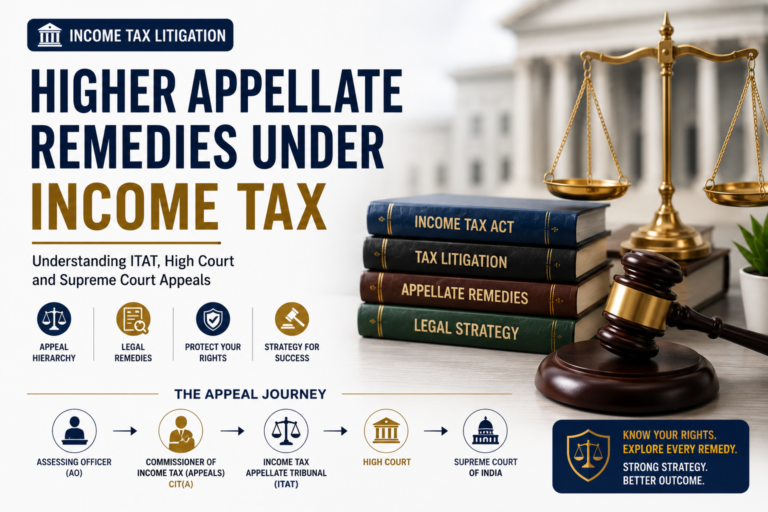

Understanding the Appeal Flow Under Income Tax

Before understanding the structure, it is important to know how the process begins.

The general flow is:

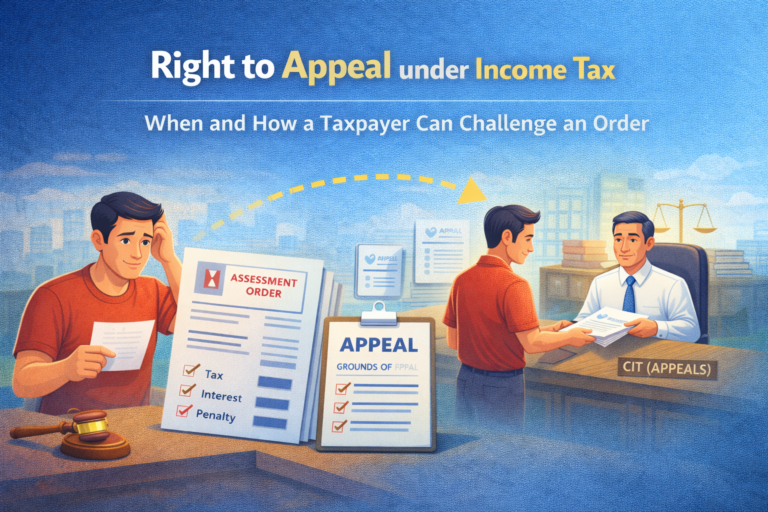

Assessment Order → Disagreement → Appeal → Commissioner of Income Tax (Appeals)

When an Assessing Officer (AO) passes an order and the taxpayer disagrees with it, the taxpayer has the legal right to challenge that order before the Commissioner of Income Tax (Appeals).

However, the appellate authority does not decide based on emotions or assumptions. It requires a properly structured appeal.

This is why:

Appeal = Structure + Clarity + Evidence

Statement of Facts: The Foundation of the Appeal

The first and one of the most important parts of an appeal is the Statement of Facts.

This section acts as the foundation of the case.

What should be included?

- Background of the case

- Nature of the transaction

- Return filing details

- Scrutiny proceedings

- Actions taken by the Assessing Officer

- How the dispute arose

Important Rule:

This section should only contain facts.

Avoid:

- Legal arguments

- Emotional statements

- Personal opinions

The facts should be presented in chronological order so the appellate authority can understand the complete matter clearly.

Practical Example:

A business files its return, scrutiny is initiated, and the AO makes an addition for unexplained expenses. This sequence should be presented clearly in the Statement of Facts.

If this section is unclear, the entire appeal can lose strength.

Grounds of Appeal: The Core of the Case

Under the Structure of an Appeal under Income Tax, the Grounds of Appeal are the most critical part.

This is where the taxpayer specifically points out the errors in the assessment order.

This section should answer:

- What mistake did the AO make?

- Why is the addition incorrect?

- Which legal principle was ignored?

For example:

“The Assessing Officer erred in disallowing business expenses without proper verification of supporting records.”

Important drafting principles:

- Keep it short

- Be specific

- Use clear legal language

- Avoid unnecessary narration

Strong grounds of appeal create the legal backbone of the case.

Supporting Documents: Evidence Strengthens the Appeal

An appeal without documentary support is often weak.

Supporting documents help establish the factual correctness of the taxpayer’s claims.

Common documents include:

- Invoices

- Bank statements

- Agreements

- Tax computation

- Ledger copies

- Audit reports

- Proof of deductions

Practical Scenario:

If an expense is disallowed by the AO for lack of evidence, the taxpayer must provide invoices and payment proofs to establish genuineness.

In tax litigation, documents often carry more weight than explanations.

Legal Submission: Applying Law to Facts

Once facts and evidence are presented, the next step is legal interpretation.

This part is known as Legal Submission.

Here, the taxpayer explains:

- Relevant provisions of the Income Tax Act

- Interpretation of applicable sections

- Judicial precedents (if relevant)

- Why the assessment order may be legally incorrect

In simple terms:

Facts + Law = Strong Appeal

For example, if a deduction is disallowed under a wrong interpretation of Section 37(1), the legal submission can clarify the actual applicability of the provision.

This section connects practical facts with legal principles.

Prayer: Clearly State the Relief Required

The final section of an appeal is the Prayer.

This is where the taxpayer clearly states what relief is being sought.

Possible reliefs may include:

- Deletion of addition

- Reduction of tax demand

- Cancellation of penalty

- Correction of disallowance

Example:

“The appellant respectfully prays for deletion of the addition made towards unexplained expenditure.”

A clear prayer helps the appellate authority understand the exact outcome being requested.

Common Mistakes in Appeal Drafting

Many appeals become weak because of drafting errors rather than legal weakness.

| Mistake | What It Means | Possible Impact |

|---|---|---|

| Unclear Facts | Incomplete, disorganized, or confusing case background | Makes it difficult for the appellate authority to understand the dispute properly |

| Vague Grounds of Appeal | General or poorly drafted objections without clear legal points | Weakens the legal strength of the appeal |

| Missing Supporting Documents | Failure to attach invoices, bank records, agreements, or evidence | Reduces credibility and factual support of the case |

| Copy-Paste Drafting | Using generic appeal drafts without case-specific details | Important facts and legal issues may be overlooked |

| Ignoring Filing Timelines | Delay in filing the appeal within prescribed time limits | May require condonation of delay and can create procedural hurdles |

Why Proper Appeal Structure Matters in Tax Litigation

A properly drafted appeal improves:

- Clarity of the case

- Understanding by appellate authority

- Presentation of facts

- Legal strength

- Procedural compliance

In tax disputes, good drafting is not just paperwork—it is strategy.

Understanding the Structure of an Appeal under Income Tax helps taxpayers protect their rights more effectively.

Conclusion

The Structure of an Appeal under Income Tax is far more than a procedural formality. It is a carefully organized legal framework that combines facts, grounds, evidence, law, and relief into one coherent presentation.

A well-structured appeal improves the quality of litigation and increases clarity before the appellate authority. Whether you are a taxpayer, student, or professional, understanding this framework is essential for handling income tax disputes properly.

Tax law may seem complex, but understanding the system makes it more manageable.

Disclaimer

This article is for educational purposes only and should not be considered legal or tax advice.