Mantra & Co. - Advocate & Tax Consultant

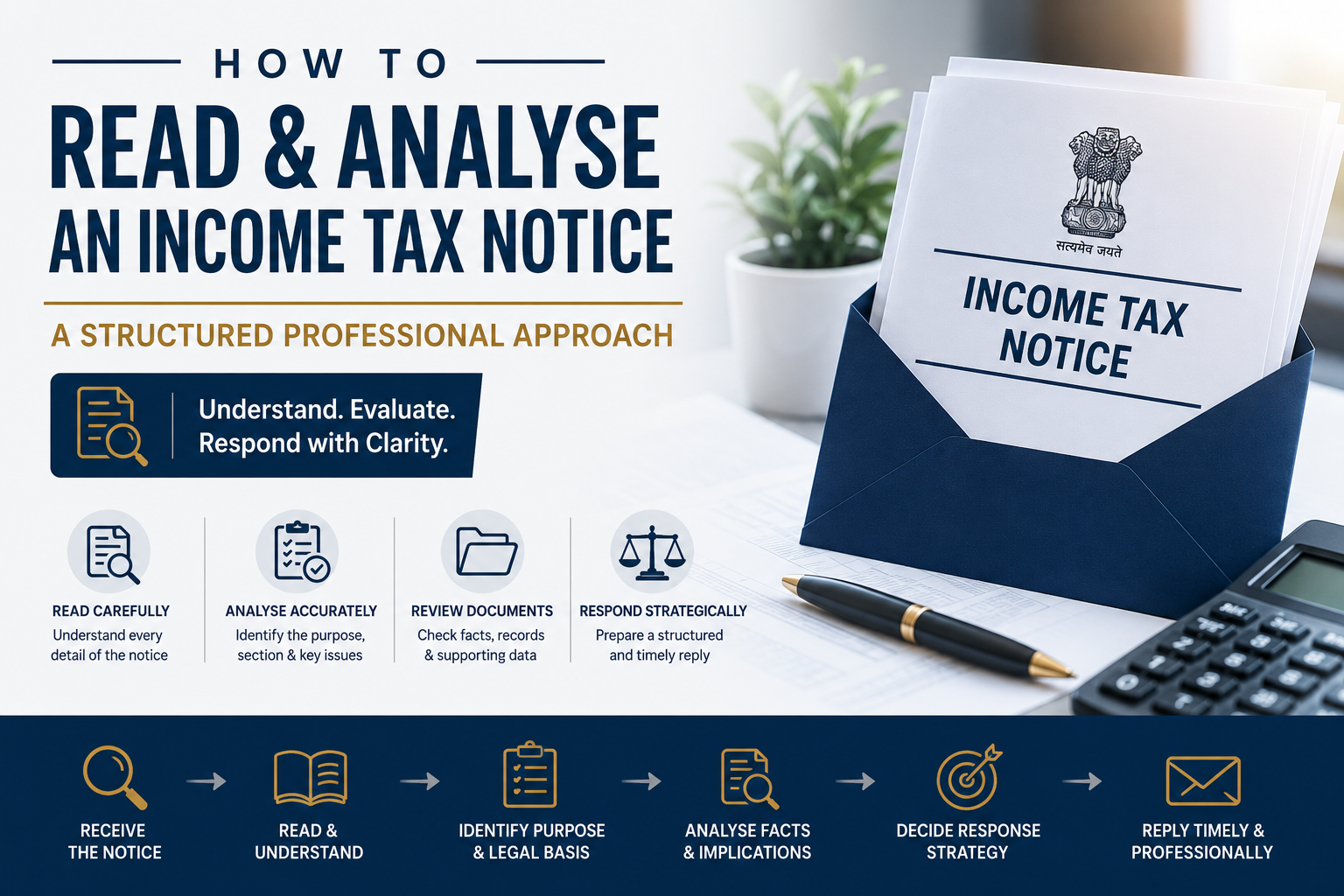

How to Read and Analyse an Income Tax Notice: A Structured Professional Approach

Introduction

Receiving an Income Tax notice does not automatically imply wrongdoing. However, misreading or misunderstanding a notice can lead to procedural errors, delayed responses, or unnecessary escalation.

For tax professionals, the ability to properly analyse a notice is a critical skill. Before drafting any reply, it is essential to understand the scope, section reference, issue involved, and compliance timeline.

This article explains a structured approach to reading and analysing an Income Tax notice.

Watch the Complete Video Explanation

This topic has also been explained in detail in the video below. Watch for practical clarity and structured understanding

Is video, we explain the entire process that takes place after filing an Income Tax Return in a simple, practical, and fear-free manner.

1. Identify the Section Under Which the Notice Is Issued

Every notice clearly mentions the section of the Income Tax Act under which it is issued.

Common examples include:

| Section 143(1) | Intimation |

| Section 139(9) | Defective return |

| Section 142(1) | Information seeking |

| Section 143(2) | Scrutiny |

| Section 144 | Show Cause Notice |

| Section 148 | Reassessment |

The section determines the seriousness and scope of the matter.

2. Understand the Purpose of the Notice

A notice may seek:

- Clarification of specific transactions

- Supporting documents

- Explanation of deductions

- Confirmation of capital gains

- Books of accounts

- Final Notice For Order to be proceeds

Professionals must clearly distinguish whether the notice is:

- Processing related

- Verification related

- Assessment related

- Reassessment related

3. Check the Assessment Year and Reference Details

Errors often occur when professionals overlook:

- Assessment year

- DIN (Document Identification Number)

- Notice date

- Response due date

Each of these details is crucial for proper compliance.

4. Review the Underlying Return and Supporting Documents

Before replying:

- Reconcile the filed return

- Review AIS and 26AS

- Examine computation sheets

- Verify books of accounts

- Prepare supporting documents

A reply should be based on facts, not assumptions.

5. Determine the Level of Risk

Not all notices carry equal weight.

| Low Risk | Medium Risk | High Risk |

|---|---|---|

| Minor mismatches | Information seeking | Scrutiny notices |

| Technical defects | Reassessment proceedings |

Professional judgment is essential at this stage.

6. Plan the Response Strategy

After analysis:

- Decide whether rectification is required

- Prepare documentary evidence

- Draft a structured response

- Maintain timeline discipline

Proper analysis prevents unnecessary litigation.

Conclusion

Reading a notice is not a clerical task. It is a professional exercise requiring legal understanding and analytical discipline.

The foundation of effective notice handling lies in accurate interpretation.

Disclaimer: This article is for informational purposes only and does not constitute legal or tax advice. The views expressed are based on the current understanding of law and portal functionality as on the date of publication. Readers are advised to seek professional advice before taking any action.

If you have any general query or wish to understand the subject better, you may share your question in the comments below.