Mantra & Co. - Advocate & Tax Consultant

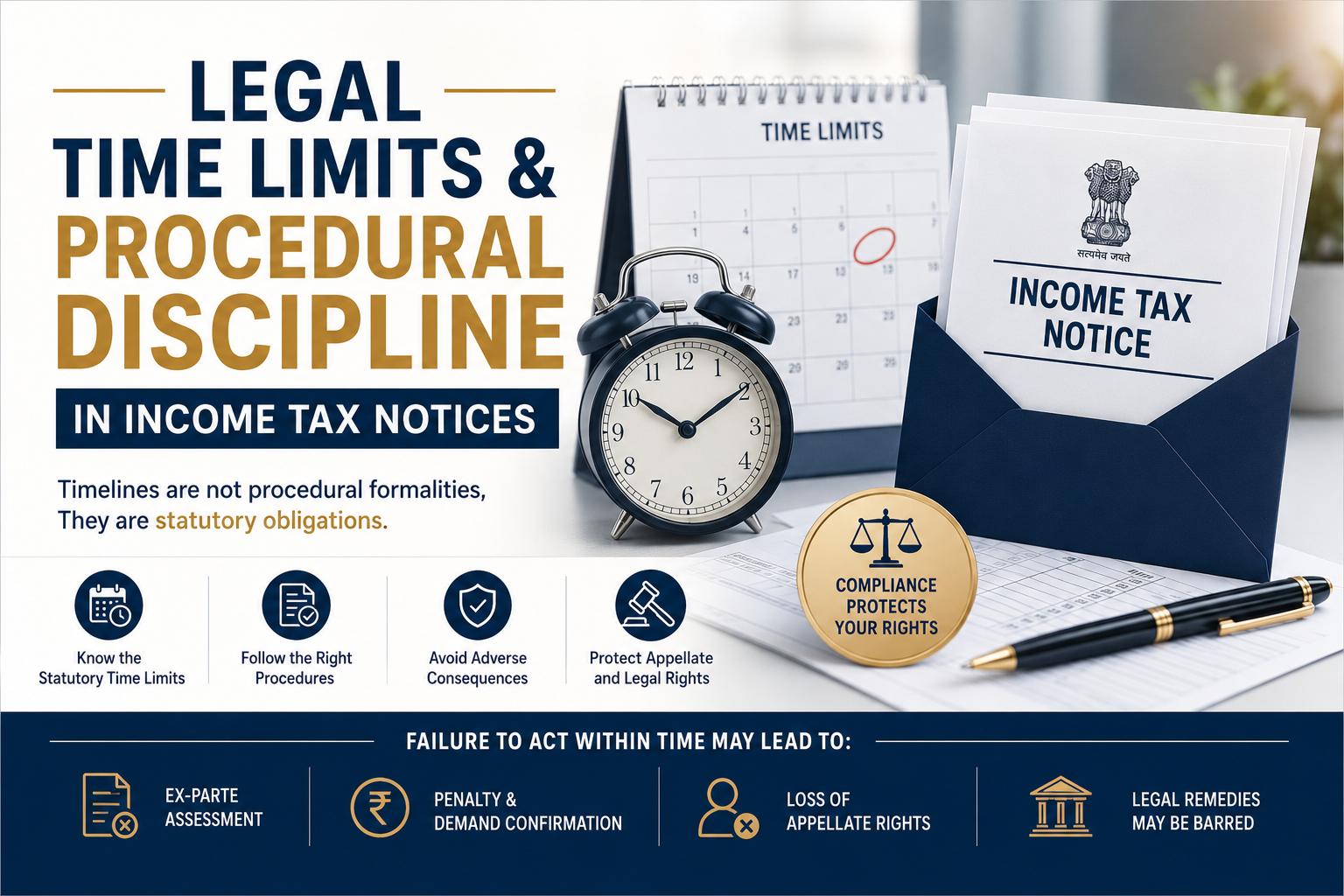

Legal Time Limits & Procedural Discipline in Income Tax Notices

Introduction

In income tax proceedings, timelines are not procedural formalities but they are statutory obligations.

Failure to observe prescribed time limits may lead to adverse consequences, including ex-parte assessment, penalty, demand confirmation, or loss of appellate rights.

For tax professionals, procedural discipline is as important as legal knowledge.

This article explains the importance of legal timelines and structured compliance discipline in handling income tax notices.

Watch the Complete Video Explanation

This topic has also been explained in detail in the video below. Watch for practical clarity and structured understanding

Is video, we explain the entire process that takes place after filing an Income Tax Return in a simple, practical, and fear-free manner.

1. Why Time Limits Matter

The Income Tax Act prescribes specific deadlines for:

- Filing responses to notices

- Filing of Income tax return u/s 148

- Submitting documents

- Filing rectification applications

- Filing appeals

- Complying with reassessment proceedings

Non-compliance within prescribed time may:

- Result in adverse orders

- Trigger penalty provisions

- Lead to prosecution in extreme cases

Timely action protects both taxpayer and professional credibility.

2. Common Notice Response Deadlines

While exact timelines vary depending on the section and facts of the case, generally:

- Notices under section 142(1) require response within the specified date mentioned in the notice

- Scrutiny proceedings under section 143(2) require compliance as per hearing dates

- Reassessment proceedings under section 148 carry strict response timelines

- Defective return notices under section 139(9) usually allow a limited rectification window

Professionals must carefully review:

- Notice issue date

- Response due date

- Mode of compliance (online/offline)

3. Consequences of Missing Deadlines

If a notice is ignored or response is delayed:

- Best judgment assessment under section 144 may be initiated

- Additions may be made without proper consideration of taxpayer explanation

- Appeal rights may become complicated

- Demand recovery may start

Procedural negligence often converts manageable issues into litigation.

4. Importance of Procedural Discipline

Professional discipline includes:

- Maintaining notice register

- Tracking response deadlines

- Keeping acknowledgment copies

- Organising digital documentation

- Maintaining communication records

A structured system prevents escalation.

5. Appeal Filing Time Limits

Appeals must be filed within prescribed timelines (generally 30 days from receipt of order, subject to condonation provisions).

Delay in filing appeal requires:

- Reasoned condonation application

- Justification for delay

- Supporting documentation

Failure to act within time may lead to dismissal.

6. Professional Responsibility

Tax practice is not only about drafting replies. It is about:

- Risk management

- Timeline monitoring

- Procedural accuracy

- Client advisory

Legal discipline defines professional maturity.

Adjournment Requests: Procedural Relief, Not a Strategy

In certain situations, a taxpayer or authorised representative may require additional time to respond to a notice.

Valid reasons may include:

- Non-availability of relevant documents

- Medical emergencies

- Requirement of third-party confirmations

- Complex reconciliation work

An adjournment request should:

- Be filed before the hearing date

- Clearly state the reason

- Be supported by brief justification

- Maintain respectful tone

Repeated or unjustified adjournments may negatively impact the officer’s perception and weaken the case.

Adjournment is a procedural relief mechanism – not a substitute for preparedness.

Conclusion

In tax proceedings, substance and procedure go hand in hand.

Ignoring timelines is often more damaging than the original tax issue.

A disciplined professional approach ensures compliance control and reduces litigation exposure.

Disclaimer: This article is for informational purposes only and does not constitute legal or tax advice. The views expressed are based on the current understanding of law and portal functionality as on the date of publication. Readers are advised to seek professional advice before taking any action.

If you have any general query or wish to understand the subject better, you may share your question in the comments below.