Mantra & Co. - Advocate & Tax Consultant

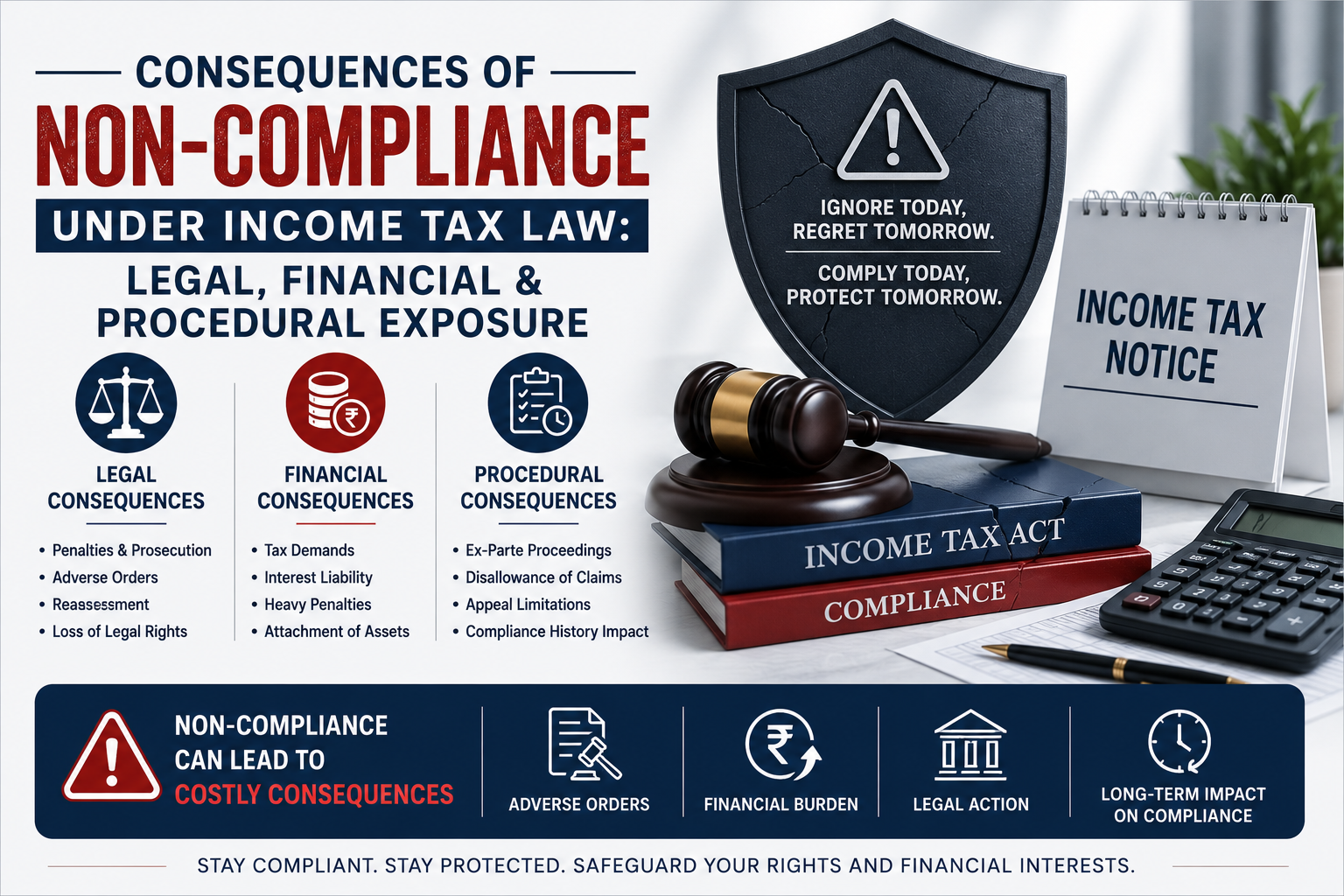

Consequences of Non-Compliance Under Income Tax Law: Legal, Financial and Procedural Exposure

Introduction

In tax practice, non-compliance is rarely a neutral event. It is often the starting point of escalation.

Many taxpayers and even junior professionals mistakenly assume that ignoring a notice merely delays proceedings. In reality, procedural non-compliance may trigger statutory consequences that are difficult to reverse.

Understanding the consequences of non-compliance is essential for risk management and professional discipline.

Watch the Complete Video Explanation

This topic has also been explained in detail in the video below. Watch for practical clarity and structured understanding

Is video, we explain the entire process that takes place after filing an Income Tax Return in a simple, practical, and fear-free manner.

1. Nature of Non-Compliance

Non-compliance may arise in different forms:

- Failure to file return within prescribed time

- Failure to respond to notice under section 142(1)

- Non-attendance during scrutiny proceedings under section 143(2)

- Failure to comply with reassessment notices

- Failure to produce books of account when required

The seriousness depends on the stage at which default occurs.

2. Best Judgment Assessment – Section 144

When a taxpayer fails to comply with statutory notices, the Assessing Officer is empowered to complete assessment to the best of his judgment.

In such cases:

- Income may be estimated

- Additions may be made based on available data

- Deductions may be disallowed due to lack of evidence

The burden shifts heavily against the taxpayer.

Once an ex-parte order is passed, rectification becomes complex.

3. Monetary Exposure: Penalty and Interest

Non-compliance may trigger:

- Penalty for failure to comply with notices

- Penalty for under-reporting or misreporting

- Late filing penalties

- Prosecution-related penalties in extreme cases

Interest under various sections is automatic and compensatory in nature. It cannot be waived merely because the taxpayer was unaware.

Financial exposure often multiplies beyond the original tax liability.

4. Impact on Litigation Position

Ignoring notices weakens future defence.

If a matter reaches the appellate stage:

- Non-cooperation history affects credibility

- Department may argue deliberate non-compliance

- Relief may become procedural rather than substantive

Procedural discipline strengthens litigation position.

5. Recovery Proceedings

Once the assessment order is passed and the demand is confirmed:

- Bank accounts may be attached

- Refunds may be adjusted

- Garnishee proceedings may be initiated

- The recovery officer may take action

At this stage, compliance options narrow significantly.

6. Professional Risk

For tax professionals:

- Missed deadlines damage reputation

- Clients may hold the advisor responsible

- Repeated defaults reduce professional credibility

Compliance management is part of professional responsibility.

Conclusion

Non-compliance transforms manageable tax queries into complex proceedings.

The safest strategy is proactive compliance, timely response, and procedural discipline.

In taxation, silence is rarely strategic.

Tax ko samajhna mushkil nahi hai,

system ko samajhna zaroori hai.

Disclaimer: This article is for informational purposes only and does not constitute legal or tax advice. The views expressed are based on the current understanding of law and portal functionality as on the date of publication. Readers are advised to seek professional advice before taking any action.

If you have any general query or wish to understand the subject better, you may share your question in the comments below.